The Hidden Dangers of Bitcoin Treasury Companies: What Smart Investors Watch For

Bitcoin treasury stocks may be the fastest way to make money in the coming gold rush, but they’re far from risk-free.

In this article, we break down the biggest threats investors need to keep an eye out for—and how to use the right tools to protect your gains.

TL;DR: What You Need to Know About BTC Treasury Risks

· BTC treasuries offer explosive upside, but come with unique risks, like mNAV implosion if BTC Yield decelerates rapidly, which can wipe out gains fast.

· High mNAVs increase drawdown risk if the company can’t maintain BTC Yield.

· Funding matters: Watch for early investors pulling out before the market tops.

· Leverage cuts both ways—debt boosts returns in bull runs but magnifies pain in bear markets.

· Leadership is critical—visionary CEOs who can be creative in their space drive long-term success and investor loyalty.

· Groupthink is dangerous—don’t mindlessly follow the hype, assuming that your bitcoin equity will keep going up forever. It’s a stock, not bitcoin, Laura.

The BTC Treasury Company Lifecycle

BTC Treasury Companies go through three phases:

1. Volatile penny stocks — with big dreams and outlandish promises.

2. Stable growth — where they put their money where their mouth is and do the hard work to source funding, gain trust and stack hard.

3. Mature BTC ‘banks’ — with slower BTC Yield and share price growth but substantial collateral that they can use to issue bitcoin-backed bonds.

It’s critical to understand which phase you’re in and act accordingly.

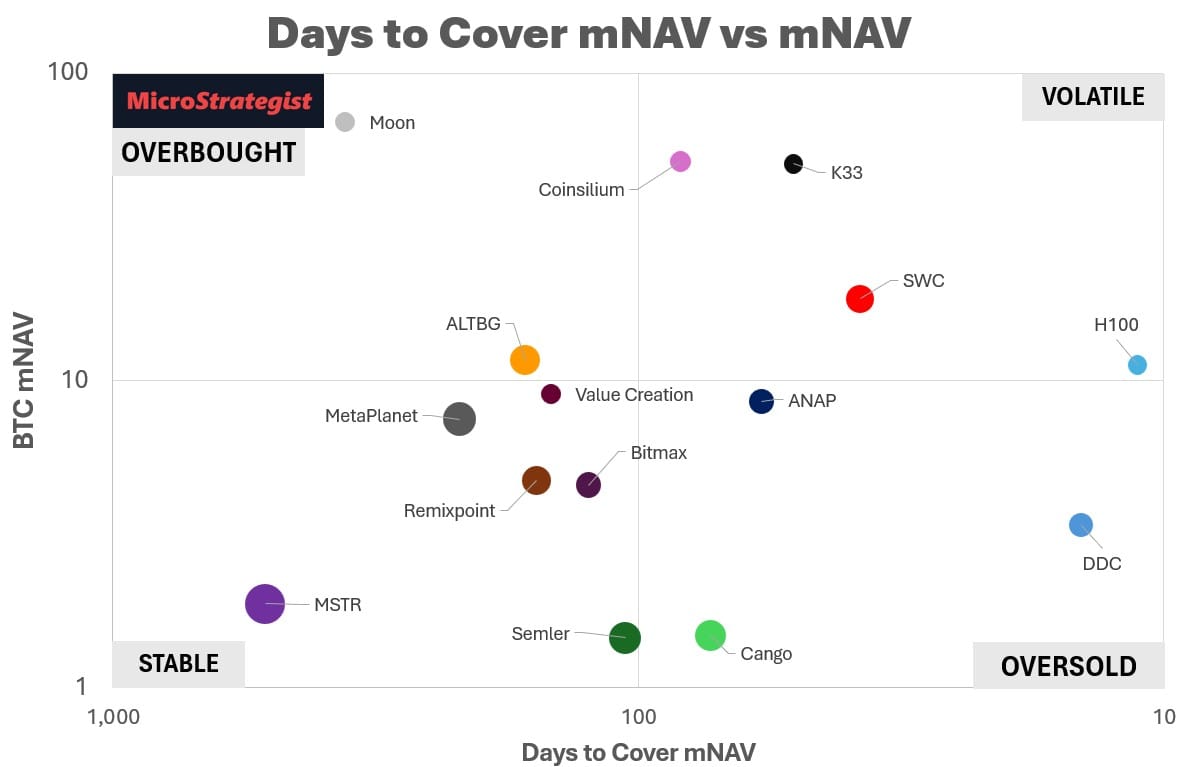

mNAV Meltdowns: The Silent Killer of BTC Stocks

The price of any BTC treasury company is the product of:

1. BTC price,

2. mNAV, and

3. BTC/share.

Share price = BTC ($) x mNAV x BTC/share

All of these things are interconnected.

But in an ideal world, they would all grow steadily together.

However, the reality is that a company can only manage its BTC/share growth, ideally while maintaining the mNAV within a healthy range (i.e., 3-5).

The mNAV is the premium that investors pay for the belief that a company will grow its BTC per share (i.e., BTC Yield). A smart BTC treasury company will structure its BTC purchases to achieve sustainable exponential growth in BTC per share for as long as possible.

It’s a Marathon, Not A Sprint

Running a BTC treasury company that grows and provides shareholder value over the long term is a marathon, not a sprint.

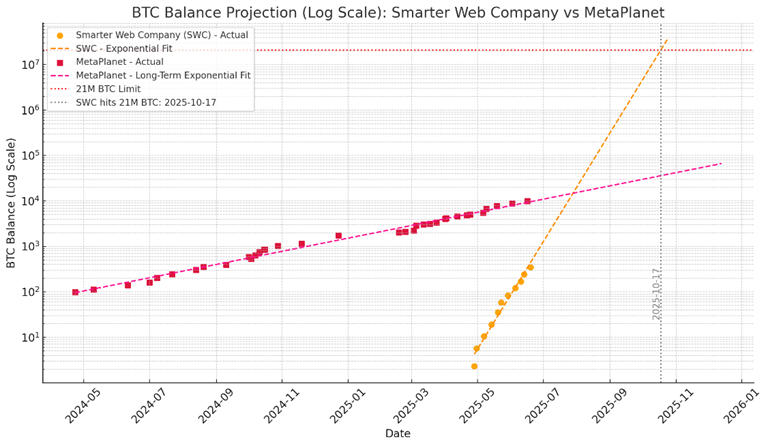

A great example of how to build a robust long-term BTC treasury is MetaPlanet, which has maintained a consistent BTC Yield of just under 1% for the long term.

As you can see in the chart below, they have plenty of room to continue to grow before running into the 21m BTC limit.

In contrast, SWC is a notable example of how to achieve massive initial, albeit ultimately unsustainable, returns. If they could continue their current BTC Yield of around 9% per day, they would hit the 21m limit on BTC in October 2025!

Investors pay a high premium (i.e. mNAV) for rapid growth (i.e. high BTC Yield). As soon as growth slows, mNAV collapses. With a current mNAV for 18, SWC have a long way to fall, especially if they fail to convert their premium to hard BTC before it’s too late.