Let the mNAV Run: Smart Play or Yield Killer for MicroStrategy?

As Strategy continues its aggressive Bitcoin accumulation strategy, investors are asking: Should they pause ATM sales and let the stock catch its breath?

While the temptation to ‘let mNAV fly’ is real, BTC Yield—not stock price—powers long-term value. MicroStrategy (aka Strategy) is walking a fine line: Should it pause ATM share sales to boost its mNAV or keep pushing for higher BTC Yield?

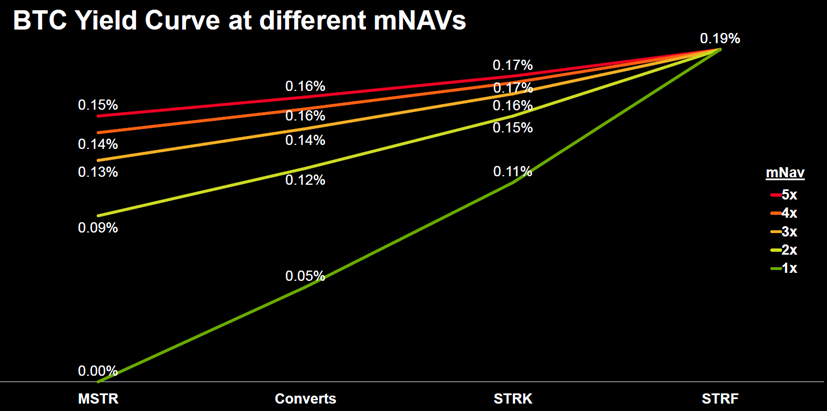

While higher mNAV excites shareholders, it’s BTC Yield that truly drives long-term value. With STRK and STRF demand still ramping up, Strategy must juggle tools like the ATM and convertibles to keep compounding Bitcoin per share.

This piece explores whether letting mNAV run could ultimately supercharge BTC Yield.

Sourcing Billions: STRK, STRF, and the ATM Machine

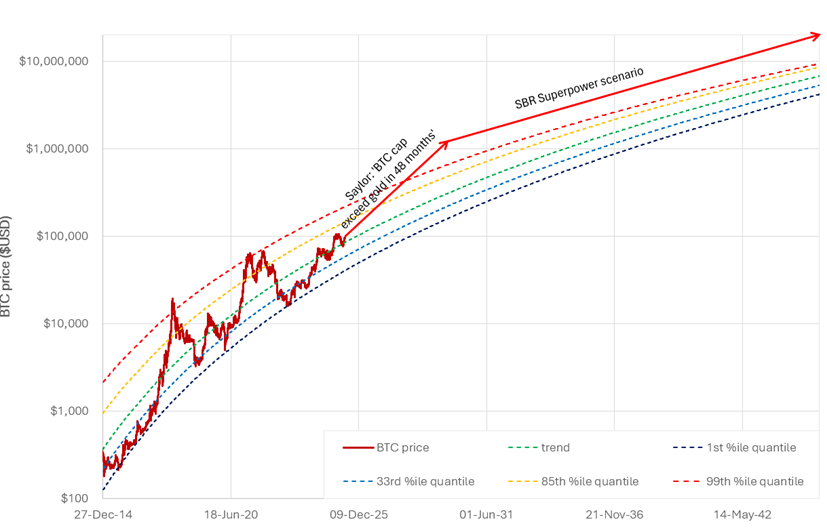

In a recent presentation, Saylor confidently stated that Bitcoin’s market cap WILL exceed Gold’s in the next 48 months and could hit $19M if the US adopts the ‘Superpower’ approach to stacking in the Strategic Bitcoin Reserve. It’s safe to say Saylor is playing the long game, trying to get as much Bitcoin as possible before the price explodes.

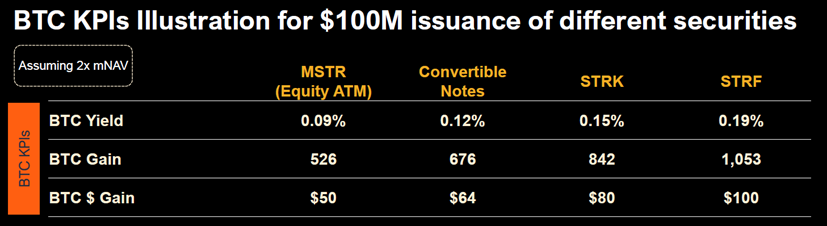

In the Strategy Q4 2025 earnings presentation, he showed that STRF and STRK are the most accretive ways to fund more bitcoin purchases. Once the volume of STRK and STRF ramps up enough to fund their bitcoin purchases, they only need to use the ATM to fund the dividends on the preferred stocks.

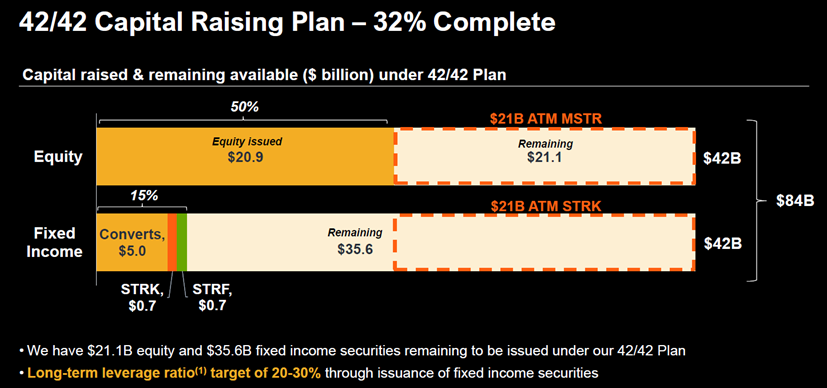

The Q1 earnings presentation also highlighted that $21B has been allocated to raising capital for STRK via ATM.

Saylor would love to see MSTR’s preferreds make up 1% of the 300T bond market. Even though Strategy’s preferred stocks have higher returns than US Treasuries, bond traders and pension funds are not yet turning to Strategy’s preferred stocks. While that may change sooner than many believe, especially with the recent US credit rating downgrade, they still need to rely on the ATM and convertible bonds for a bit longer.

The mNAV Line Strategy Won’t Cross

Saylor also highlighted in the recent earnings call that, while there’s a big difference between selling MSTR shares at an mNAV of 1 and 2, the additional benefit of waiting until mNAV is 3 or 4 diminishes.

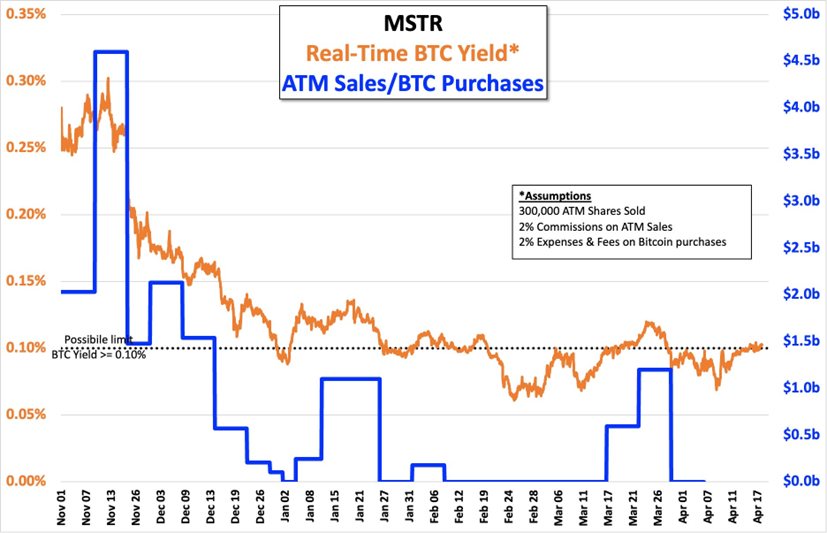

More recently, as demonstrated by this chart from @dnelson58 on X, Strategy seems to have used an mNAV of 2.0 (i.e., a BTC Yield of 0.09%) as the floor below which they’re unwilling to use the ATM, which would push the mNAV even lower.

Due to this self-imposed limit, we’ve seen weeks where Strategy cannot purchase more Bitcoin when mNAV drops below 2. Strategy are unwilling to drive the price lower.

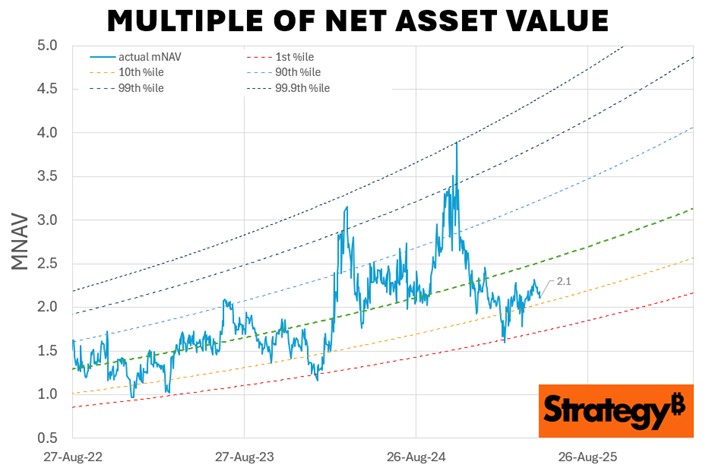

Since the start of 2022, mNAV has been trending upwards on a slow exponential curve. It’s currently at 2.1, below the November 2024 peak, but above the long-term average of 1.8.

The two previous massive peaks occurred when Bitcoin ripped after the announcement of the ETFs and the election, when people were seeking leveraged Bitcoin exposure.

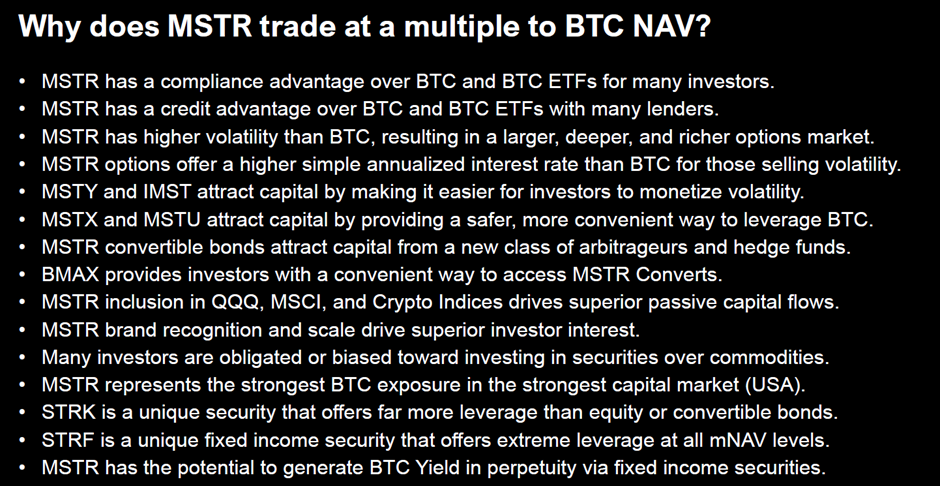

In the Q1 2025 earnings call, Saylor listed many reasons MSTR should trade with an mNAV greater than 1.0. With few viable competitors, especially with their trustworthy size and structure, Saylor believes the mNAV will continue trending up.

BTC Yield: The Real KPI That Matters

While the mNAV fluctuates in the short term, BTC Yield is the critical long-term factor.

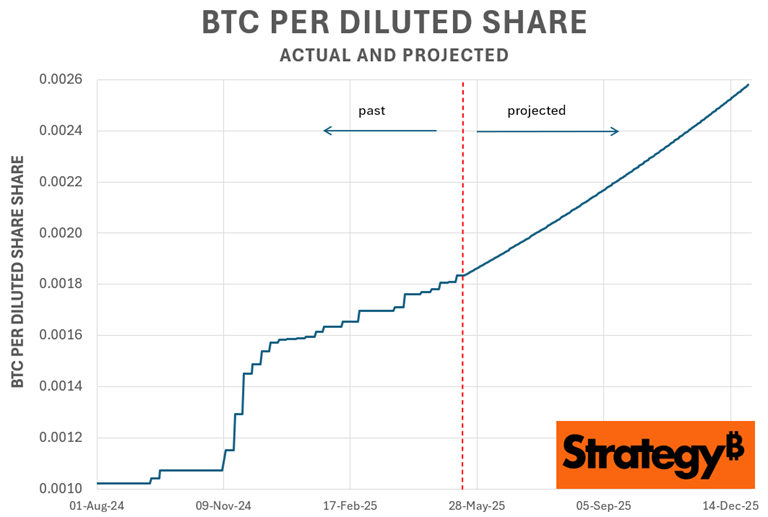

The BTC treasury company that can stack stats the fastest will ultimately see the most long-term growth in share price. Our analysis suggests that, with a current debt ratio of 19% (well below their 30% limit), they might pull off a BTC Yield of 74% p.a. for the rest of 2025. Without BTC Yield, MSTR is just another BTC ETF.

Which Lever Should MSTR Pull Next?

It’s abundantly clear that Strategy would rather be selling STRF and STRK right now, but the volume of buyers is not there yet. Lowering the price might spook new STRK buyers, but also attract yield-hunters.

So, they must alternate between the ATM and convertible bonds for now. Unfortunately, ironically, MSTR’s volatility is currently relatively low because the share price has been going straight up for the past month or so. Hence, they could not negotiate a conversion premium high enough to make the bonds sufficiently accretive.

In the meantime, the ATM helps them harvest more fiat to bring down the debt. The debt/bitcoin NAV ratio is currently at 17%, below their 20-30% target range. So one can only expect they’re lining up another convertible bond issue, ready to issue as soon as the volatility ramps up again.

The chart below shows the (debt + preferred)/BTC NAV ratio, demonstrating that their debt ratio was much higher in 2022 and 2023, making them high-risk for the big money funds they’re now trying to appeal to. They’d prefer to play things on the safe side to ensure their bonds are well over collateralised and let the newer BTC treasury companies take the gamble.

In addition to funding BTC purchases, one of the other benefits of the ATM is Strategy can hammer it to bring down the debt to make room for more convertible bonds or create a safety buffer if they think a significant bitcoin drawdown might be on the horizon.

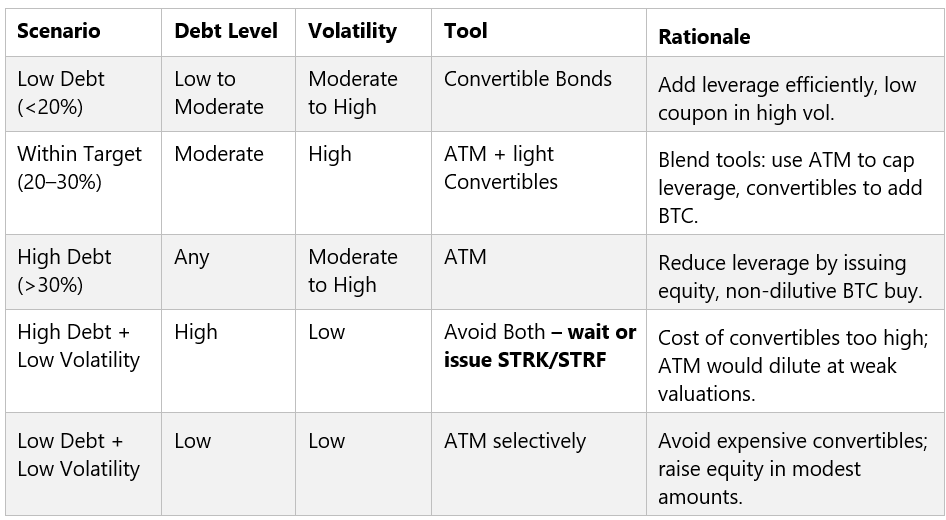

Chasing the Right Tool for the Job

So, when should Strategy use the ATM vs convertible notes vs the perpetuals to raise funds to keep growing their BTC Yield? The table below outlines a decision matrix along the lines of what Strategy are likely using.

Given Saylor is literally a rocket scientist who runs an AI and BI company, I’m sure they have some much more complex tools set up to help them maximise MSTR’s long-term returns in any situation.

BTC Yield First, Share Price Second

For shareholders, mNAV pumps feel good, but BTC Yield is what compounds wealth. Strategy’s next funding moves could define the next decade of value creation.

· In the long term, Strategy aims to transition to the more accretive perpetual shares (STRK and STRF), but the volume is not yet high enough to rely solely on these.

· While backing off the ATM for a few months might help the share price pump in the short term, BTC Yield is Strategy’s #1 KPI to maximise long-term value creation.

· The ATM (at the market share sales) enables Strategy to de-leverage when volatility is lower and when the mNAV is above 2.0, making room on the balance sheet for more convertible debt when volatility picks up.