Mapping the Lifecycle of a Bitcoin Treasury Company: From Hype to Hard Collateral

Bitcoin treasury companies follow a distinct lifecycle: they start in the top right of our chart—small but explosive—and, ideally, drift slowly but steadily toward the bottom left, loaded up with as much BTC as possible to wield as hard collateral in the financial system of the future.

Whether you’re an investor chasing the next wave in the BTC treasury gold rush or dreaming of launching your own version of MSTR, MetaPlanet, or SWC, this framework will help you navigate the ride.

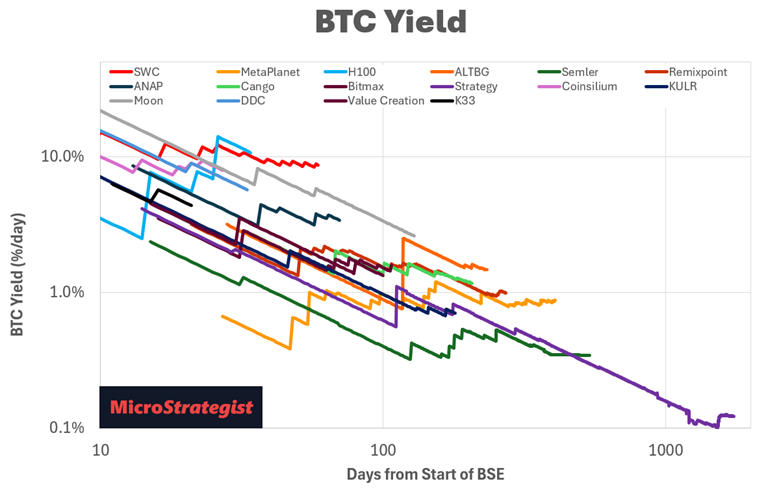

Start Here: Smaller Stack, Greater Yield

BTC Yield is a function of your current stack. The smaller your starting point, the higher your potential yield.

Day 1: Buy 1 BTC. That’s it.

From there, you plot a sustainable trajectory.

Sure, you could go for a 10% daily BTC Yield and look like a legend for a minute.

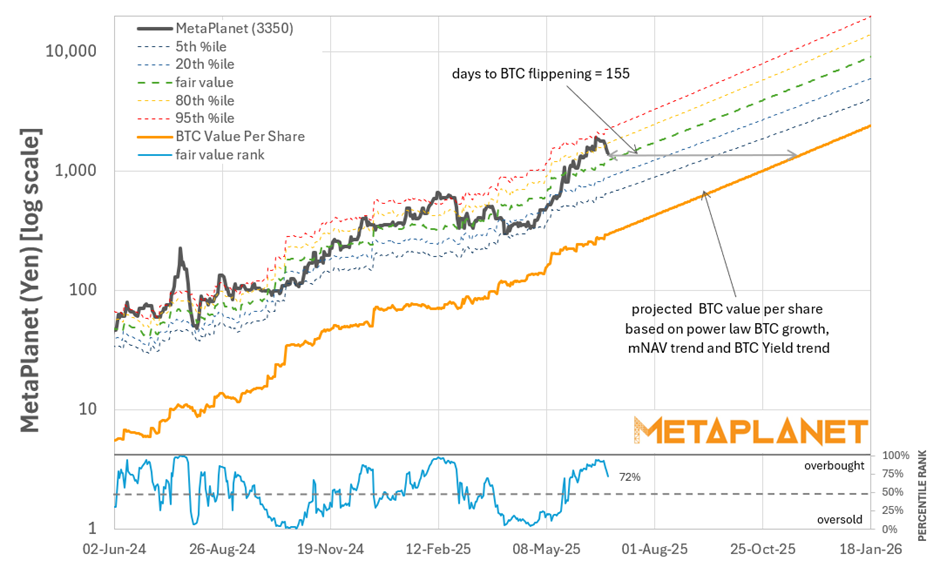

But if you’re thinking long-term survival and durable compounding power, a modest 1% daily yield (like MetaPlanet) might be a smarter play.

Choose a Sustainable Launch Trajectory

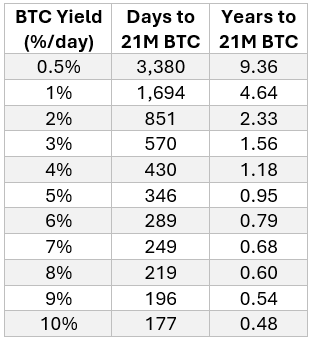

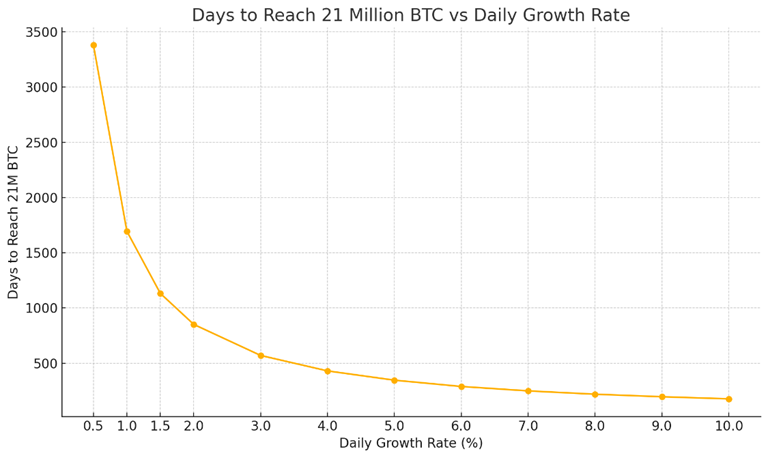

A 1% daily BTC Yield doesn’t sound too flashy—but compound it, and things get wild, setting you on the path to snap up all 21m BTC in 4.6 years.

However, if you’re running a 10% daily BTC Yield, your entire lifecycle is under six months. That’s not a robust treasury—it’s a supernova. Something has to break, sooner rather than later.

Currently, several new BTC treasury companies are riding the 10% rocket BTC Yield. If you’re investing in one of them, watch for a slowdown in BTC Yield. When funding dries up, the mNAV will compress fast.

Phase 1 – Hype & Seed Capital

The first step is the ignition phase.

A few big BTC buys from well-connected insiders, press releases, and podcast appearances generate the initial buzz.

This drives a high BTC Yield, which in turn attracts the retail FOMO flywheel.

The result?

Price and mNAV soar.

Phase 2 – At-the-Market (ATM) Selling

As retail piles in, price and mNAV continue to climb.

Before early investors start taking profits, a smart BTC treasury company will fire up the ATM facility to sell their shares at a premium. This is where you convert the hype into hard BTC.

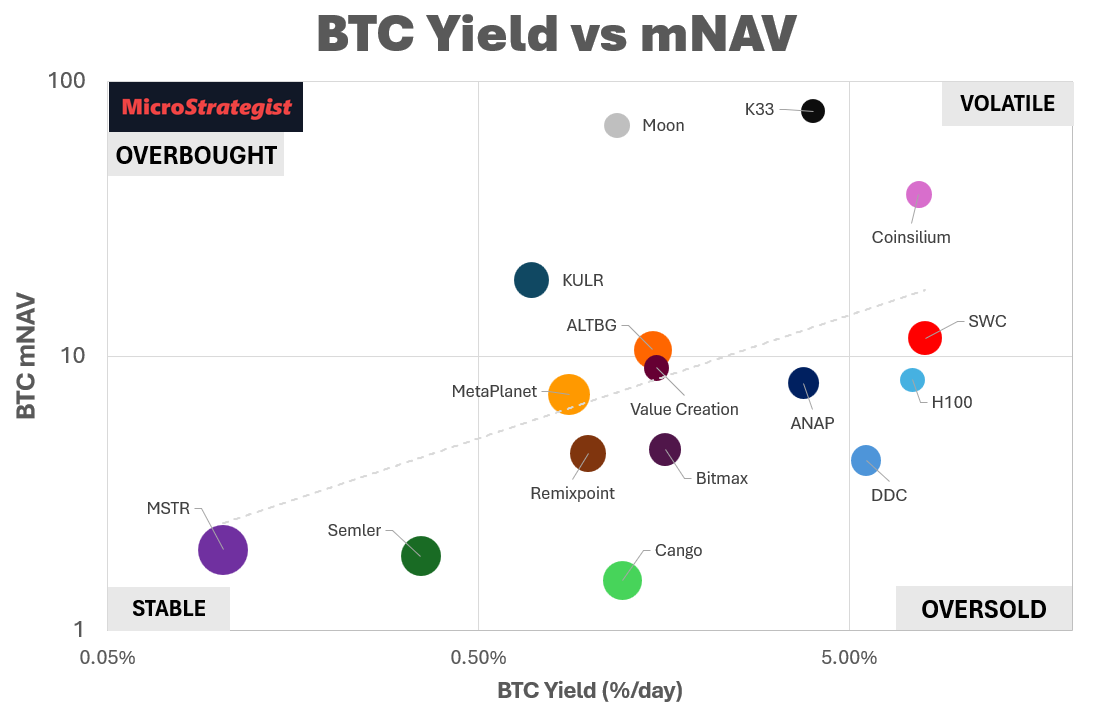

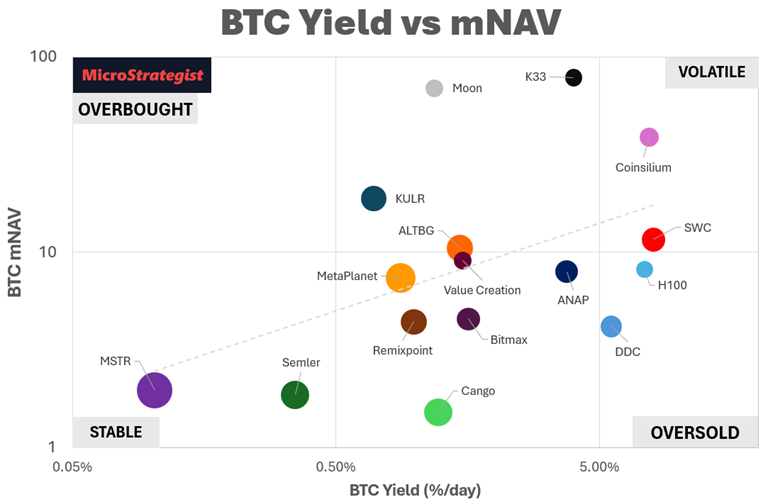

Done right, ATM selling becomes the engine room of ongoing BTC accumulation. It funds the next leg up, driving them down and towards the bottom right on our bubble chart (BTC Yield vs mNAV chart) below.

Smart Capital Rotation

With dozens of BTC treasury companies now in the race, capital will naturally rotate, in search of the best bang for their buck.

Investors:

· Load up on companies below the trend line—cheap BTC per share with plenty of upside from higher BTC yield.

· Avoid buying companies with a high mNAV too far above the trend line, especially if you think their BTC Yield might be about to stall.

BTC Treasury Companies

· Sell shares aggressively when you drift above the trend line.

· But let mNAV drift too high without action, and capital will rotate to newer, faster-growing players before you can capture the premium and convert it to digital gold.

This cycle keeps the company’s BTC value per share rising while maintaining a healthy BTC Yield.

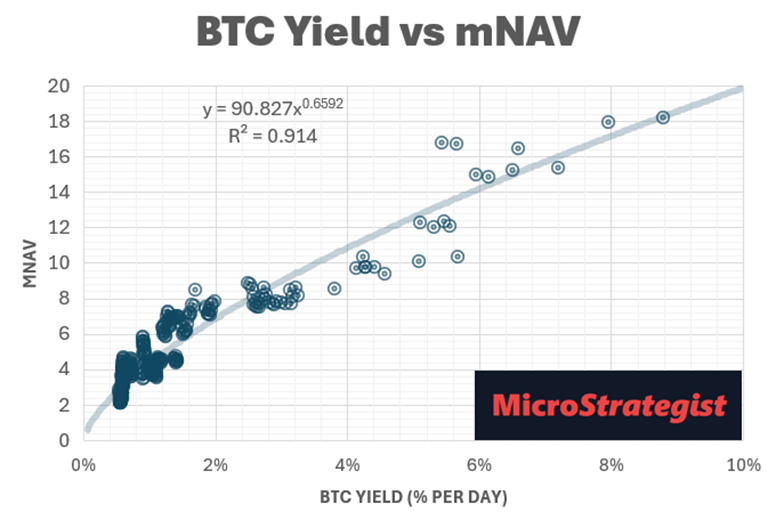

BTC Yield Is Everything

Investors pay a premium (mNAV) for BTC Yield. However, the larger the BTC stack gets, the more difficult it becomes to maintain that yield.

BTC Yield = new BTC added / current BTC stack

If liquidity for the ATM dries up or exchange access limits capital flow, BTC Yield falls. And when BTC Yield falls, mNAV collapses.

If you can’t hold mNAV above 3, the ATM becomes more dilutive, so you’d better have dry powder ready. Otherwise, you’ll need to pivot—fast.

Preferred Shares or Bust

The final form for BTC treasury companies?

Selling preferred shares to bond investors.

Strategy is already leading with STRK, STRF, and STRD. Others will follow. Before long, investors will be comparing yields and risk profiles of the various BTC treasury companies, just like they do with government bonds.

Those with massive BTC stacks and minimal debt—like Strategy and MetaPlanet—will dominate.

But for others, if no one’s buying your preferreds, BTC Yield will continue to fall, and mNAV will trend to 1, making you a zombie BTC treasury company, ripe for acquisition.

The Biggest Risk Isn’t Leverage—It’s mNAV Compression

Everyone worries about debt and the subsequent default of BTC treasury companies.

But the real risk is failing to sustain BTC Yield over the long term.

Take MSTR. Even after buying mountains of BTC, their mNAV halved (from 4 to 2) last year after a short spike in BTC Yield.

Why?

BTC Yield couldn’t keep up with the size of the stack, and mNAV fell.

Currently, we have smaller companies with astronomical mNAVs, which is justified if they can maintain a high BTC yield.

But buyer beware: if they cannot maintain it, mNAV will plummet.

If you buy a company that’s currently running hot with a BTC Yield of 10% and an mNAV of 20, and its BTC Yield suddenly drops to 1%, the mNAV will fall from 20 to 4 (i.e. an 80% drop in stock price).

Bottom line: Sustainable BTC Yield is the key to long-term success. Go too hard, too fast, and you'll burn your investors as the yield inevitably cools.

Key Takeaways

· The higher the BTC Yield, the faster a company moves through its lifecycle.

· Falling BTC Yield leads to imploding mNAV and falling share price.

· Small BTC treasury companies can grow fastest but can also crash the hardest.

· Prudent BTC Treasury Companies use ATMs to extend the high-yield phases.

· Retail will chase rocket yields; institutions will buy them out later.

· The endgame is preferred shares—bond-like stability backed by BTC as collateral.

It’s going to be a wild ride.

Strap in.

We’ll be here with the charts and tools to help you navigate every twist and turn.