The Lookback Edge: How Optimising Yield Windows Turned 5x into 59x

Everyone agrees that BTC Yield — the change in bitcoin per share — is the ultimate scorecard for Bitcoin Treasury Companies (BTC-TCs). But what often goes unnoticed is how we measure it. The length of the lookback window — whether 30 days, 90 days, or a full year — can completely change the signal.

Too short, and the data looks like static. Too long, and you risk hanging on as a company runs out of steam and its mNAV collapses. The difference isn’t academic — it can be the line between riding a 59x winner or watching your gains evaporate.

In this article, we’ll show how optimising the yield lookback period transforms our ability to spot rockets early, cut losers quickly, and balance risk across the BTC-TC portfolio.

This isn’t about changing the companies you pick — it’s about changing how you measure them. A better lookback transforms noise into signal, and signal into returns.

The Signal-to-Noise Problem

“BTC Yield” (i.e. change in BTC/share for a BTC-TC) is commonly agreed to be the most important metric that a BTC-TC should focus on.

But the lookback period that we calculate BTC Yield over matters – too short, and the signal is super noisy. Too long, and you risk hanging on too long as the BTC-TC dies and mNAV implodes.

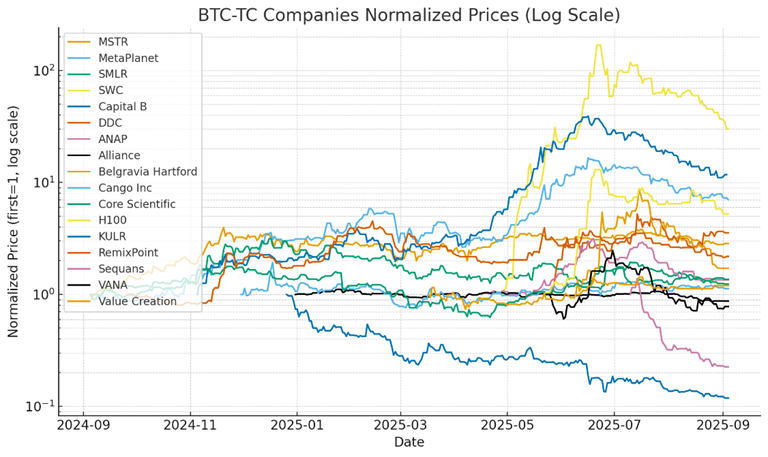

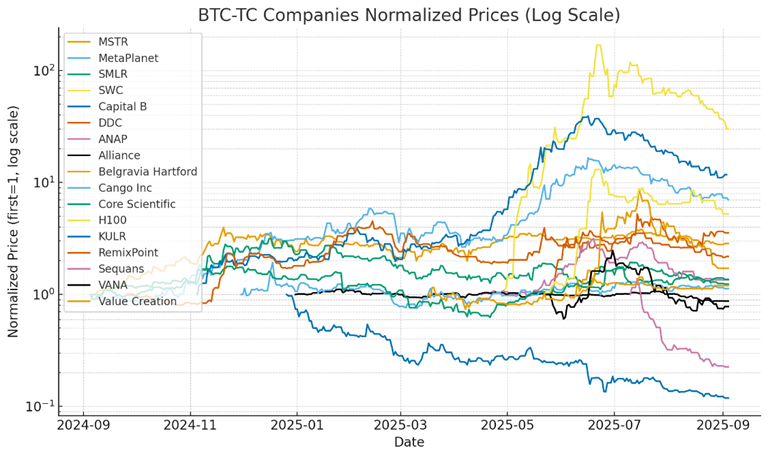

The chart below shows the normalised price of the BTC-TCs we’re tracking. While some have made incredible gains, others have crashed and burned, particularly over the past couple of months.

The BTC-TC sector has seen a massive pullback since the peak on 22 June 2025. But on the upside, we now have some real data to help us refine our system to identify which BTC-TCs are about to tank.

Static vs Adaptive BTC Yield Windows

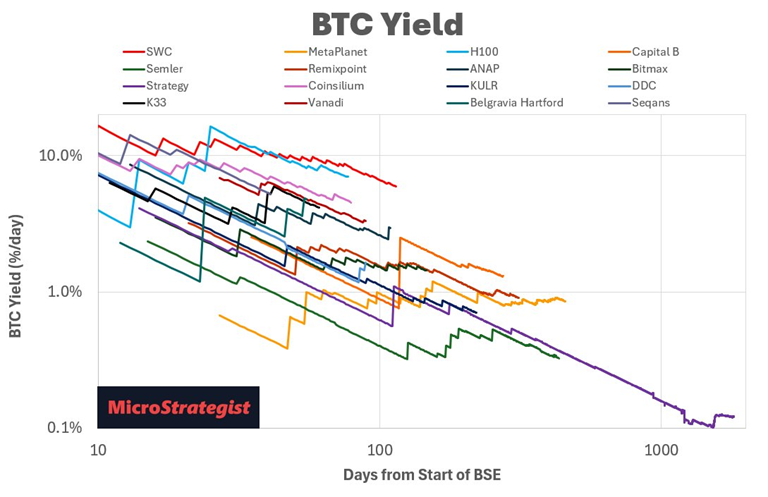

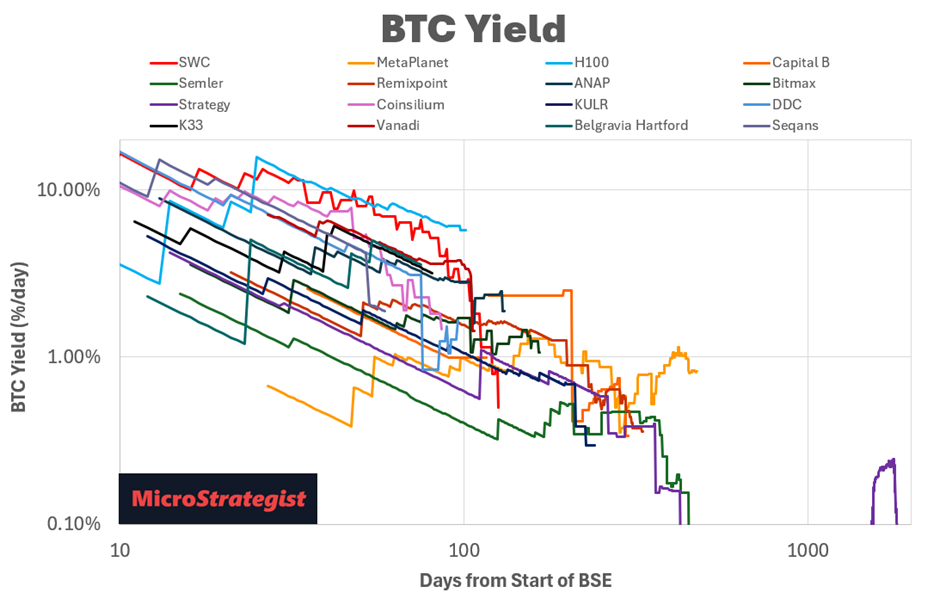

To date, we’ve been using BTC Yield based on the time since the company started actively stacking BTC (to), as shown in the chart below.

The advantage of this approach is that it is robust and straightforward. No discretionary judgment is required. However, the disadvantage is that it’s not as responsive to when a company starts to slow or accelerate their stacking.

But after an exchange with Ragnar on X, I thought it would be worth digging into the optimal lookback period a little more. I’ve tried to do this manually in Excel previously, but this time I found ChatGPT could nail the optimisation and backtesting process.

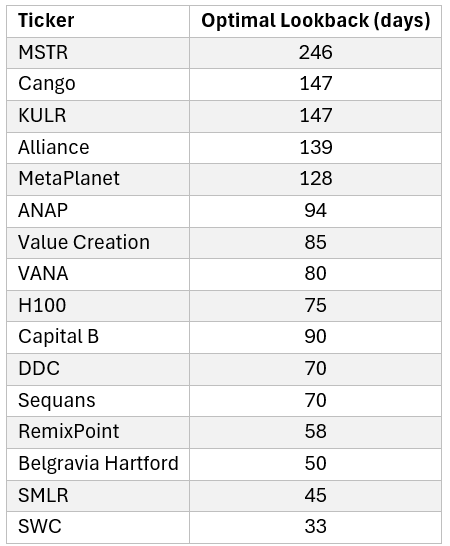

The table below shows the optimal lookback period identified by the analysis. Notice how the rockets (SWC, Belgravia) need tight 30–60 day windows, while veterans like MSTR need a much longer leash.

This contrast underscores why a one-size-fits-all approach fails — different companies demand different windows.

· When a new company starts stacking, we have to use their first day (to).

· However, for companies that are growing extremely rapidly, we have to be alert to the fact that they will inevitably slow down, and their mNAV will likely collapse. Hence, we need to keep them on a tight leash with a shorter lookback period. We want to know as soon as possible whether the rocket that we have chosen is headed for the moon or it’s about to fall out of the sky.

· Meanwhile, a longer lookback period makes sense for companies that have a demonstrated history of consistent stacking.

The chart below shows the updated BTC Yield vs time with the optimised lookback periods. The updated BTC Yield chart below shows BTC Yield calculated using the optimised lookback periods.

While it’s messier, it is more responsive and lets us know sooner if there’s a problem brewing. While companies can claim lofty goals for accumulating Bitcoin, talk is cheap. To protect our risk, we need to monitor the actual data to see when they’re actually running out of steam.

Under the Hood: How the Model Works

For the quant nerds, let’s take a look at the components of the system.

BTC Yield

BTC Yield is the same as we’ve used before, just with a defined lockback window. We’re calculating the yield over the last L days, not just from the beginning of their stacking.

DTC mNAV

Days to Cover mNAV is still the number of days it will take for the company to earn back its current mNAV premium. But this time, we’re considering the BTC Yield over a certain amount of time.

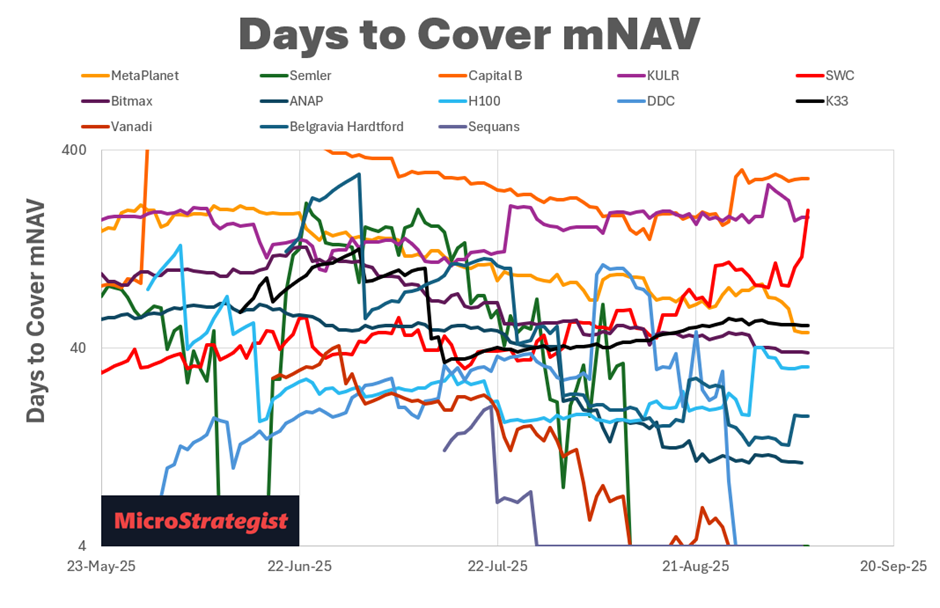

The chart below shows the DTC mNAV with the optimised lookback. While a bit messier with the shorter-term lookbacks, it’s more responsive to the actual rate of stacking. Every day without a BTC buy means their DTC mNAV drifts up a little more.

Portfolio weighting

We can then use this to create a weighted portfolio based on the inverse of DTC mNAV. Companies with a lower DTC mNAV receive a higher weighting. However, we unwind these positions as the mNAV rises, the BTC Yield slows, or the mNAV becomes too high.

One Size Doesn’t Fit All

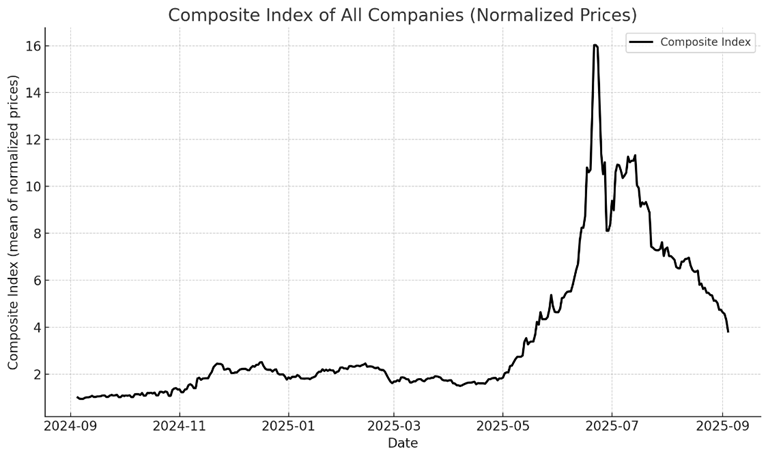

Back in May, we ran a portfolio backtest using the inverse of DTC mNAV, which showed an incredible 100x in a year. But over that period, everything was going up – the system just switched to the next fastest horse when it emerged. But over the past couple of months, we’ve seen some brutal drawdowns in BTC-TCs. We now have data that helps us understand what a BTC-TC looks like when it’s starting to roll over.

While some companies have pulled back more than others, we’ve seen a massive drawdown. While this hurts BTC-TC investors right now, the upside is that we now have real-life data that helps us fine-tune our system to navigate similar pullbacks in the future.

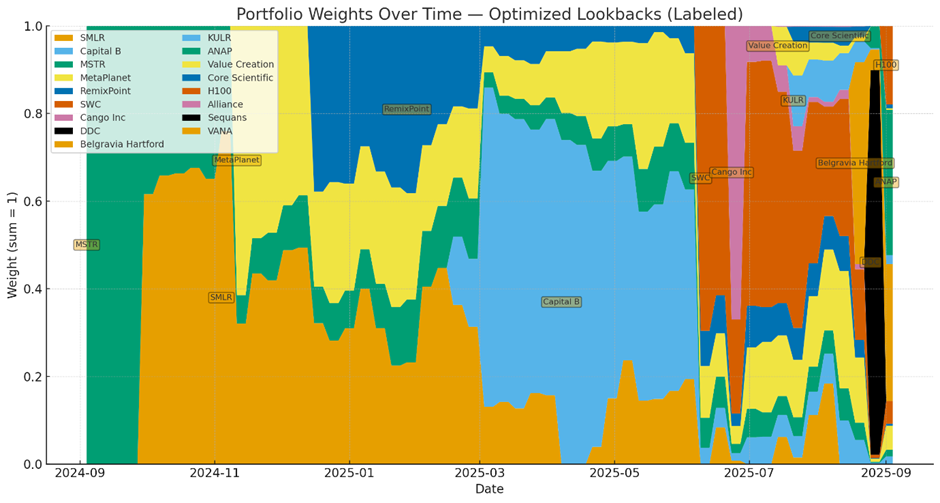

The chart below shows how the system rotates through different BTC-TCs based on their DTC mNAV. A year ago, the system was 100% invested in MSTR, but then it diversified to invest in SMLR, MetaPlanet and Capital B as they came along. Later, it jumps heavily into SWC as it pops along with the other rockets for a time, but exits at the first sign of slowing BTC Yield.

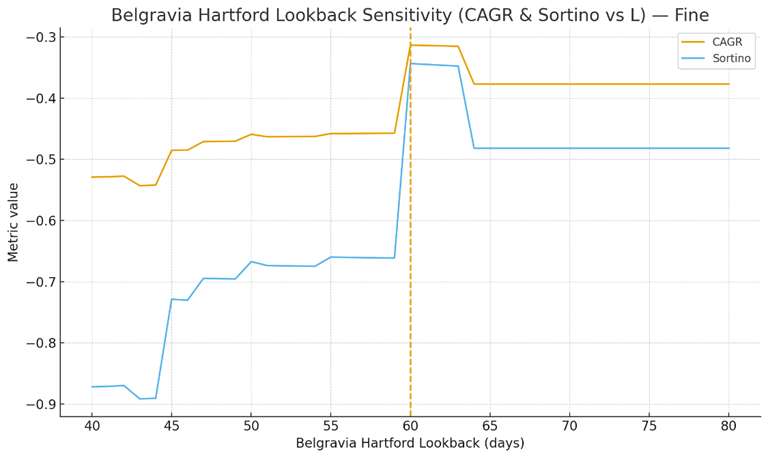

I initially ran a global optimisation, but then we optimised each company’s look-back period one at a time and locked in rational values. As shown in the chart below, a shorter (60-day) lookback is ideal for Belgravia Hartford, which is a smaller, faster-moving BTC-TC, so we want to know as soon as their stacking starts to slow.

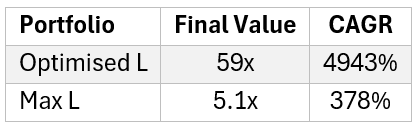

The Payoff: 5x or 59x?

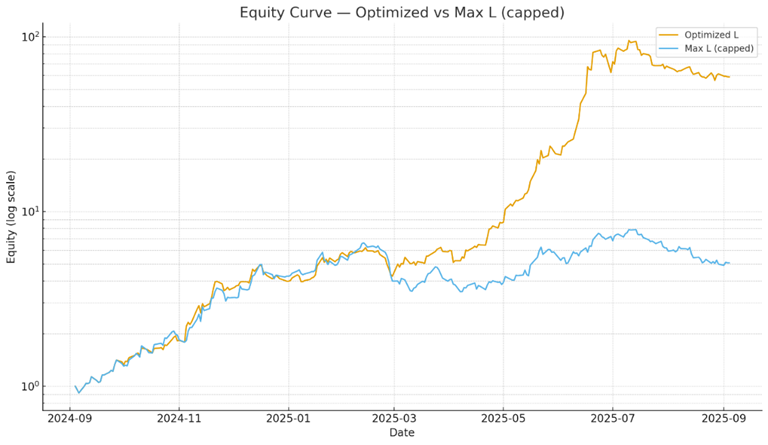

And the chart below shows the equity curves before and after optimising for the lookback period, optimised to maximise the Sortino ratio (i.e. CAGR/max drawdown).

The non-optimised version gives an impressive 5.1x return (CAGR = 378% p.a.), even after the recent drawdown. However, the optimised portfolio gives us a super impressive 59x return (CAGR = 4943% p.a.), even after the recent drawdown.

While this is definitely ‘curve fitting’ and it would be hard to repeat these returns going forward in real life, it’s helpful to validate the system and confirm that using a shorter lookback period for faster-moving BTC-TCs is valuable.

Of course, past optimisation doesn’t guarantee future performance, but it sharpens our playbook for when the next cycle arrives.

Conclusion: Keeping the Rockets on a Tight Leash

BTC Yield remains the single most important metric for Bitcoin Treasury Companies. But as we’ve seen, the timeframe we use to measure that yield can make the difference between catching a rocket early or being left holding wreckage.

For the fast movers, shorter lookbacks of 60–90 days give us the responsiveness we need to see when momentum stalls. For the steadier stackers, longer windows provide the grace they deserve to demonstrate consistency before we rotate out.

By tuning the lookback period to each company’s stacking profile, we get a system that’s not only more adaptive but also more protective of capital when the tide turns. The last few months of drawdowns have been painful, but they’ve also given us real-world data to sharpen our tools.

The next cycle will separate rockets from wreckage. With an adaptive lookback, you won’t just watch from the ground — you’ll know when to climb aboard, and when to eject.